- Blog

- /

- How Open Banking Is Streamlining Loan Approvals for Small Businesses

How Open Banking Is Streamlining Loan Approvals for Small Businesses

Estimated Read Time: 5 Minutes

Pooja Jaiswal , 26 March, 2025

Access to capital still stands as one of the formidable barriers to small business growth. SMEs often encounter stiff lending criteria under a long list of paperwork for loan applications, alongside prolonged wait times for approval. Traditional lenders employ outdated credit models, making it difficult for SMEs to provide a strong case for their financial viability.

The emergence of Open Banking (OB) is transforming this landscape. Today, the sector is moving in a positive direction towards faster data-oriented lending evaluations.

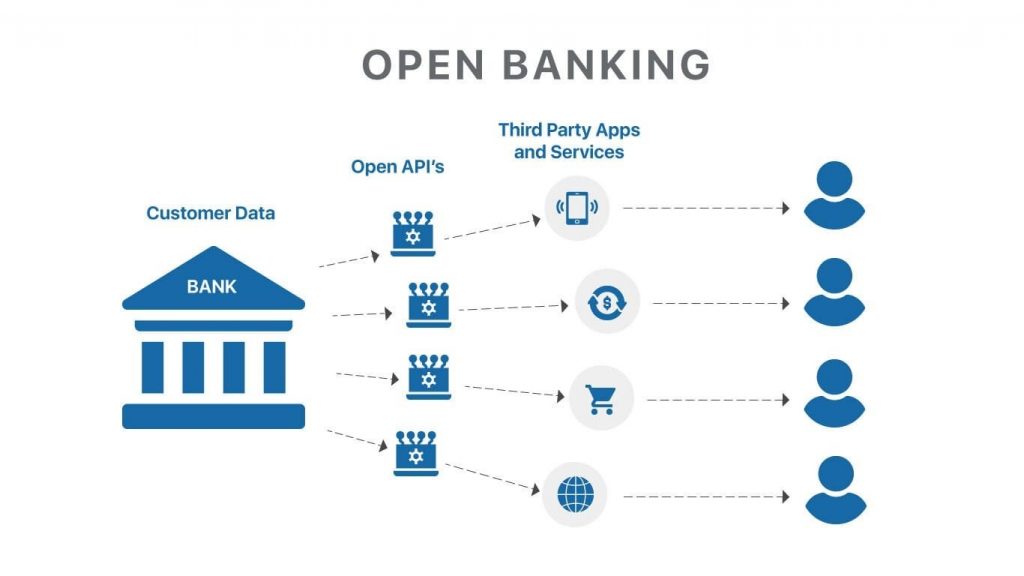

Understanding Open Banking

OB provides access through APIs that enable banks and financial services companies to share account access with third-party approved providers. It also protects client information. This initiative aims to provide an environment conducive to more competition and innovation.

A Brief History of Open Banking

Based on regulatory reforms, OB promotes transparency and competition in financial services. The EU’s PSD2 (Revised Payment Services Directive) and the UK’s Open Banking Initiative, which was initiated in 2018, opened the door for companies to share financial information securely with permitted third-party providers.

OB has only become more robust internationally since, ensuring that there is greater efficiency and inclusion of SME finance. Open Banking market internationally reached a revenue of USD 25,137.1 million in 2023 and will reach USD 135,173.8 million by 2030, signifying the market’s rapid development and change-oriented ability.

Small businesses can leverage OB to easily assess risk more accurately and reduce reliance on outdated credit scoring models. This shift speeds up loan approvals with automated, and real-time financial insights. It ensures quick access to more tailored financial products and financing options when they need them most.

The Role of APIs in Real-Time Financial Data Exchange

APIs play an important role in Open Banking. It enables banks, fintech platforms, and lending institutions to exchange standardised data seamlessly. Real-time access allows lenders to assess a business’s financial health almost immediately, moving away from outdated credit scores and static financial reports.

Business Loan Approval Challenges Faced by Small Businesses

Common Challenges

- Lack of Collateral: Many small firms do not possess sufficient assets to offer as collateral. Which makes them struggle to secure traditional loans.

- Poor or Insufficient Credit History: Most start-ups and small-scale businesses either have poor credit histories or no credit history at all; thus, it is difficult for them to get loans.

- Inconsistent Cash Flow: Irregular income streams can make lenders wary of approving loans.

- Lengthy and Complex Application Processes: Loans with banks involve complicated and long application processes which can deter small and medium enterprises from applying.

- High Interest Rates: SMEs are charged high interest rates compared to big ones because they are believed to involve more risks.

Less Common but Significant Challenges

- Industry-Specific Risks: Certain industries are considered riskier, creating more challenges in lending for SMEs in these particular industries.

- Economic Conditions: A macroeconomic adverse scenario for credit would restrict access to finance for SMEs.

- Regulatory Changes: Changes in financial regulations would create some ambiguity that influences loan approval.

- Geopolitical Risks: SMEs operating in less politically stable areas have a higher deal of difficulty in accessing loans.

How Open Banking Helps Small Businesses Overcome These Challenges

For small businesses, OB can eliminate many traditional roadblocks in securing finance. OB provides safe, real-time access to financial information, which breaks the focus away from fixed credit scores and collateral-based lending and moves towards a dynamic and more transparent evaluation of business health.

Rather than fighting through cumbersome approval procedures, small businesses can offer a transparent, fact-based financial picture that speaks for itself. Lenders can evaluate the merit of loan requests more accurately, taking into account real-time cash flow information instead of historical credit history. This translates to firms with thin credit histories or fluctuating seasonal revenue no longer being automatically disqualified.

The result? Faster approvals, less paperwork, and better access to funding. By eliminating unnecessary friction in the lending process, OB ensures that SMEs get the financial support when they need it most.

How Nucleus Supports SMEs with Open Banking

Nucleus leads the way in using Open Banking to streamline SME loan approval. Through safe access to financial information, they assess company wellbeing more precisely, going beyond outdated credit scores and collateral demands. This facilitates quicker decision-making and more bespoke financial products.

Nucleus provides adjustable business loans that conform to the specific financial position of SMEs. Their hassle-free method provides lower paperwork, faster approvals, and better visibility into cash flows. By embedding Open Banking insight, Nucleus is able to detect cash shortages and design personalised solutions that equip businesses to develop with needed funds without redundant delay.

For small businesses, seeking efficient and transparent funding, Nucleus combines technology and financial expertise to create a lending experience that matches the pace of modern business. Contact us today to explore the right funding options for your business.