- Blog

- /

- A Step-by-Step Guide For Commercial Loan Applications

A Step-by-Step Guide For Commercial Loan Applications

Estimated Read Time: 5 Minutes

Pooja Jaiswal , 16 September, 2024

Getting a commercial loan can be quite the game-changer for any business wanting to expand and succeed. But let’s get real here: the whole process of just a loan application might feel really overwhelming. Thankfully, we’ve prepared a straightforward guide to take you through all the necessary steps.

Importance of Commercial Loan Applications

Businesses understand the critical importance of commercial loans as they align with the business’s future. To navigate through this crucial process, businesses must familiarise themselves with the intricacies of loan applications. This proactive approach will not only raise the chances of securing the loan but also improve creditworthiness, and relationship with the lenders.

Essential Documents Required for Commercial Loans

Below is the documentation required for lenders to evaluate the eligibility of the borrower.

Note: Documentation may differ from lender to lender.

Key Financial Criteria

When approving loans, lenders follow critical financial criteria to evaluate the borrowers. Below are a few key factors lenders analyse, that you can use to strengthen your loan applications.

Financial Statements

Your creditors determine your current economic health through financial reports. You are encouraged to maintain and update your financial statements for the last 2-3 years, which also include cash flow statements, a balance sheet, an income statement, and a P&L statement. These documents assess lenders to decide whether to lend or not.

Creditworthiness

The credit score denotes the borrowers’ repaying capability. It reflects the financial history, and therefore the borrowers should be prepared with the documents that show the financial stability of the business entity concerning its repaying capability.

Debt-to-Income Ratio (DTI)

It basically represents how much debt you have against your income. Lenders use it to determine your borrowing risk. Although a DTI of 43% is typically the highest ratio, a borrower can have and still get qualified for a loan, but lenders generally seek ratios above 36%.

Formula for DTI:

Source: Net Debt Formula

Here’s how it works:

- Sum up your monthly debt payments (including credit cards, car loans, and mortgages).

- Divide this total by your gross (pre-tax) monthly income.

- Multiply the result by 100 to get the DTI ratio as a percentage.

Collateral and Personal Guarantee

Collateral refers to the asset or property kept as security for the loan. Lenders typically prefer property as their most preferred collateral, but business equipment, machinery, invoices or other assets can also be used as collateral. Lenders may also ask for a personal guarantee, holding the borrower liable to repay the loan if it fails. Collateral and Personal Guarantee requirements are essential for the loan process.

Business Plan

Crafting a well-structured business plan is highly recommended. Lenders may require comprehensive business key performance data to comprehend the business’s objectives, strategies, and precise financial insights which will eventually lead them to success.

Cash Flow

A cash flow statement reflects a business’s health, and positive cash flow indicates the healthiness of the business. It also provides an avenue for a business to make relevant decisions regarding its growth and expansion. Lenders are more confident in borrowers with positive cash flow, which simultaneously enhances their chances of loan approval.

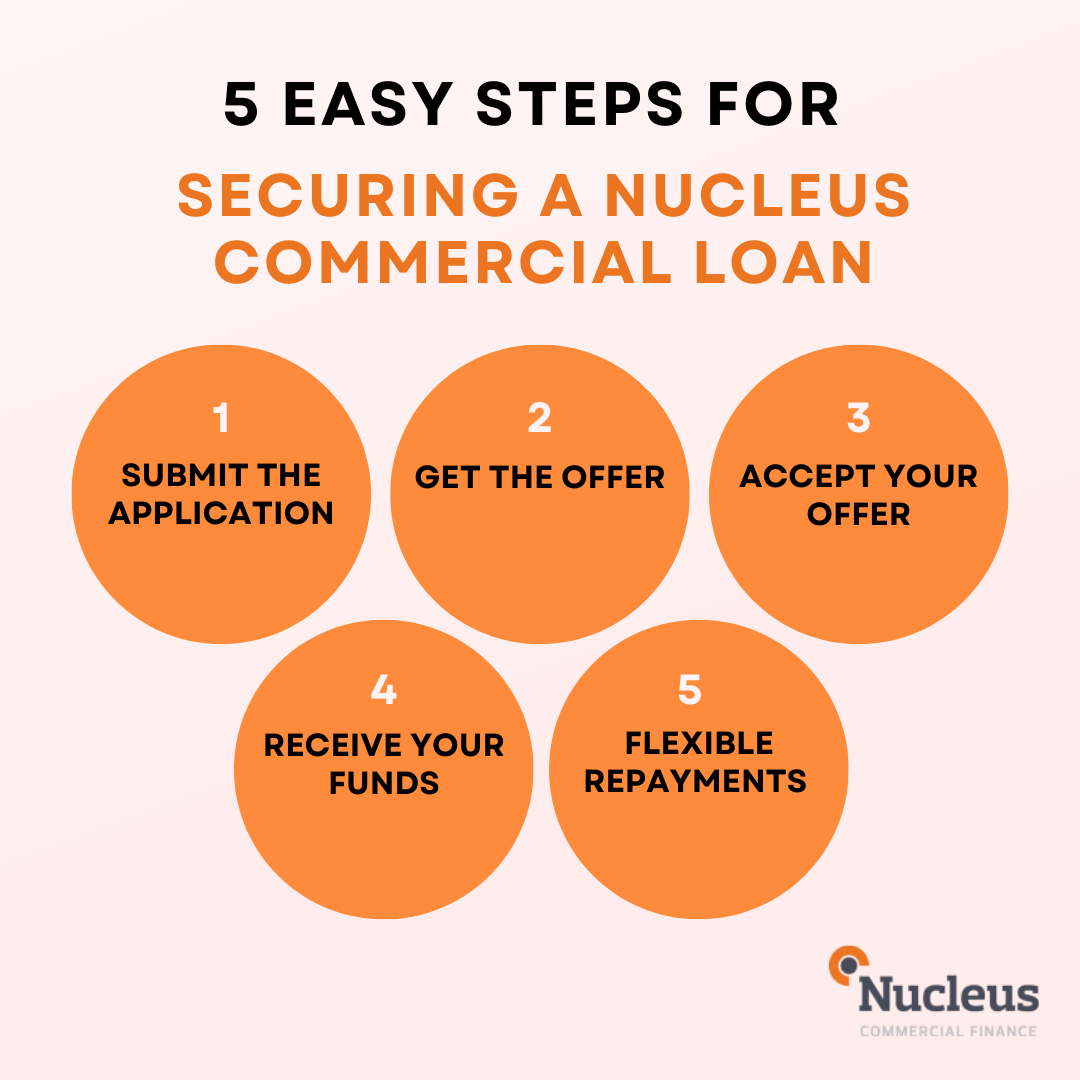

5 Easy Steps for Securing a Nucleus Commerical Loan

Step 1: Submit the Application

Before submitting the application, make sure which loan type aligns best with your business goals. Once you decide on the loan type, submit your online application which requires essential details such as business information, trading information, loan information and personal details.

Documents required:

| Loan Type | NBL (Nucleus Based Loan) | RBL (Revenue Based Loan) |

| Eligibility | Minimum 12 months trading history. At least one Director based in the UK. | Your business has been trading for at least 4 months. At least 1 Director must be based in the UK. Be clearing a minimum of 10 transactions per month. Have access to Open Banking. Be backed by personal guarantees. |

| Documents | Access this product via Open Banking and Open Accounting. | As we require Open Banking access on all revenue-based loans, decisions are instant. Legals and a DocuSign link will then be sent immediately should you wish to proceed. |

Step 2: Get the Offer

Once you submit the application with Nucleus, our AI-powered system processes your application quickly. This efficient system allows Nucleus to quickly evaluate your application and generate loan offers based on your financial profile and needs.

Step 3: Accept Your Offer

Once you receive the offer, you can decide upon whether to go ahead with the agreement. If you choose to move forward, you can sign your documents remotely and effortlessly on any device, anytime ensuring a seamless and effortless process.

Step 4: Receive Your funds

After finalising the agreement and completing the paperwork, Nucleus releases the funds directly to your business account, enabling quick fund access and smooth functioning to achieve your business objectives.

Step 5: Flexible Repayments

We offer straightforward repayment options to make loan management hassle-free. We provide fixed, weekly direct debits, which simplifies the budgeting process and ensures that repayments are made consistently and on time.

Conclusion

Commercial loans are valuable for businesses seeking to secure financial stability and growth. With key knowledge about different types of commercial loans and their application process, businesses can make informed decisions, craft efficient business plans, build stronger relationships with lenders and increase loan approval chances. Explore how Nucleus can simplify this process and assist many businesses like retailers, cafes, properties, manufacturers and more such success stories. Apply now and take your business to new heights.